Risk Stewards: Cap Adjustments on Aave V3 / 2026.04.30

Asset Info

CreatorN/A

Registration TimeLoading...

RegistrarRisk Stewards: Cap Adjustments on Aave V3 / 2026.04.30

Capture TimeLoading...

GeolocationN/A

File TypePNG

Source TypedigitalUpload

Details

Abstract

Summary

LlamaRisk recommends the following parameter changes based on user behavior, on-chain liquidity, and position health observed in the latest review of Aave V3 reserves.

Aave V3 Ethereum Core:

Increase supply cap for USDG from 60,000,000 to 120,000,000.

Increase borrow cap for USDG from 50,000,000 to 100,000,000.

Increase supply cap for PT-USDG-28MAY2026 from 40,000,000 to 80,000,000.

Reduce borrow cap for USDe from 1,800,000,000 to 360,000,000.

Aave V3 MegaETH:

Increase supply cap for USDe from 50,000,000 to 100,000,000.

Increase supply cap for USDm from 400,000,000 to 600,000,000.

Increase borrow cap for USDm from 190,000,000 to 280,000,000.

Aave V3 Celo:

Increase supply cap for USD₮ from 5,800,000 to 11,600,000.

Aave V3 X Layer:

Increase borrow cap for xETH from 1,300 to 2,600.

Aave V3 Plasma:

Reduce borrow cap for WETH from 8,000 to 4,000.

Aave V3 Mantle:

Reduce borrow cap for USDe from 72,000,000 to 27,000,000.

USDe (Aave V3 MegaETH)

USDe has reached 100.0% supply cap utilization (50,000,000 / 50,000,000) on the Aave V3 MegaETH instance.

Supply Distribution

Source: LlamaRisk, April 30, 2026

The dominant usage pattern is a leveraged stable-stable loop: USDe collateral against USDm debt under the stablecoin E-Mode. Health factors among active borrowers cluster between 1.04 and 1.09, with a smaller cohort holding USDe on a passive deposit basis (HF infinite). The tight HF cluster reflects capital-efficient looping; collateral and debt are both USD-pegged stablecoins, so liquidation risk is contained.

Recommendation

Given full cap utilization, the structurally low liquidation risk of the correlated stablecoin loop, and persistent demand on the MegaETH instance, we recommend doubling the supply cap from 50,000,000 to 100,000,000. The borrow cap remains unchanged.

USDm (Aave V3 MegaETH)

USDm is currently at 59.2% supply cap utilization (236,684,728 / 400,000,000) and 17.2% borrow cap utilization (32,771,432 / 190,000,000) on the Aave V3 MegaETH instance. The reserve is configured with LTV 0% and cannot be used as collateral. Borrowing is enabled.

Supply Distribution

Source: LlamaRisk, April 30, 2026

Top USDm suppliers hold the asset on a passive deposit basis, with health factors predominantly at infinity across the depicted set. As a non-collateral asset, USDm contributes no liquidation pathways on the supply side, so the cap governs reserve size rather than collateral concentration. On the borrow side, the looped pattern observed on the USDe reserve consumes USDm liquidity, and borrow utilization is expected to expand as the USDe supply cap doubles to 100,000,000. It is notable that currently the reserve is highly concentrated, with 1 address accounting for more than 80% of the reserve.

Recommendation

Given the planned USDe supply cap raise on the same instance and the corresponding expansion of the USDe / USDm correlated stablecoin loop, we recommend increasing the USDm supply cap from 400,000,000 to 600,000,000 and the USDm borrow cap from 190,000,000 to 280,000,000. The supply-side raise has no collateral-related liquidation pathway as the asset is not allowed as collateral, and the borrow-side raise is sized to absorb expected growth in demand and market borrow capacity.

USDG (Aave V3 Ethereum)

USDG is currently at 84.2% supply cap utilization (50,504,894 / 60,000,000) and 84.7% borrow cap utilization (42,342,061 / 50,000,000) on the Aave V3 Ethereum instance. Borrowing of the asset is enabled.

Supply Distribution

Source: LlamaRisk, April 30, 2026

Top USDG suppliers hold the asset on a passive deposit basis, with health factors at infinity throughout the depicted set. Demand for USDG borrowing originates from positions collateralized by other reserves and does not appear in this chart. The supply leg therefore operates as a yield-bearing dollar deposit, and the supply-side concentration profile is not a liquidation channel.

Recommendation

Given that both supply and borrow caps are utilized above 84% and that the supply leg shows no leveraged usage that would convert headroom into liquidation risk, we recommend doubling both caps: supply cap from 60,000,000 to 120,000,000 and borrow cap from 50,000,000 to 100,000,000.

PT-USDG-28MAY2026 (Aave V3 Ethereum)

PT-USDG-28MAY2026 has reached 80.9% supply cap utilization (32,378,236 / 40,000,000) on the Aave V3 Ethereum instance.

Supply Distribution

Source: LlamaRisk, April 30, 2026

The dominant usage pattern is a leveraged carry trade: PT-USDG collateral against USDG, USDC, and USDe debt under the stablecoin E-Mode. Health factors among active borrowers cluster between 1.00 and 1.06, reflecting capital-efficient looping where the PT and the borrowed stablecoin are both pegged to the dollar. The HF cluster is consistent with low liquidation risk because the principal-only payoff of the PT is fixed in USDG terms at maturity, and the residual price risk before maturity is bounded by the AMM-implied yield curve.

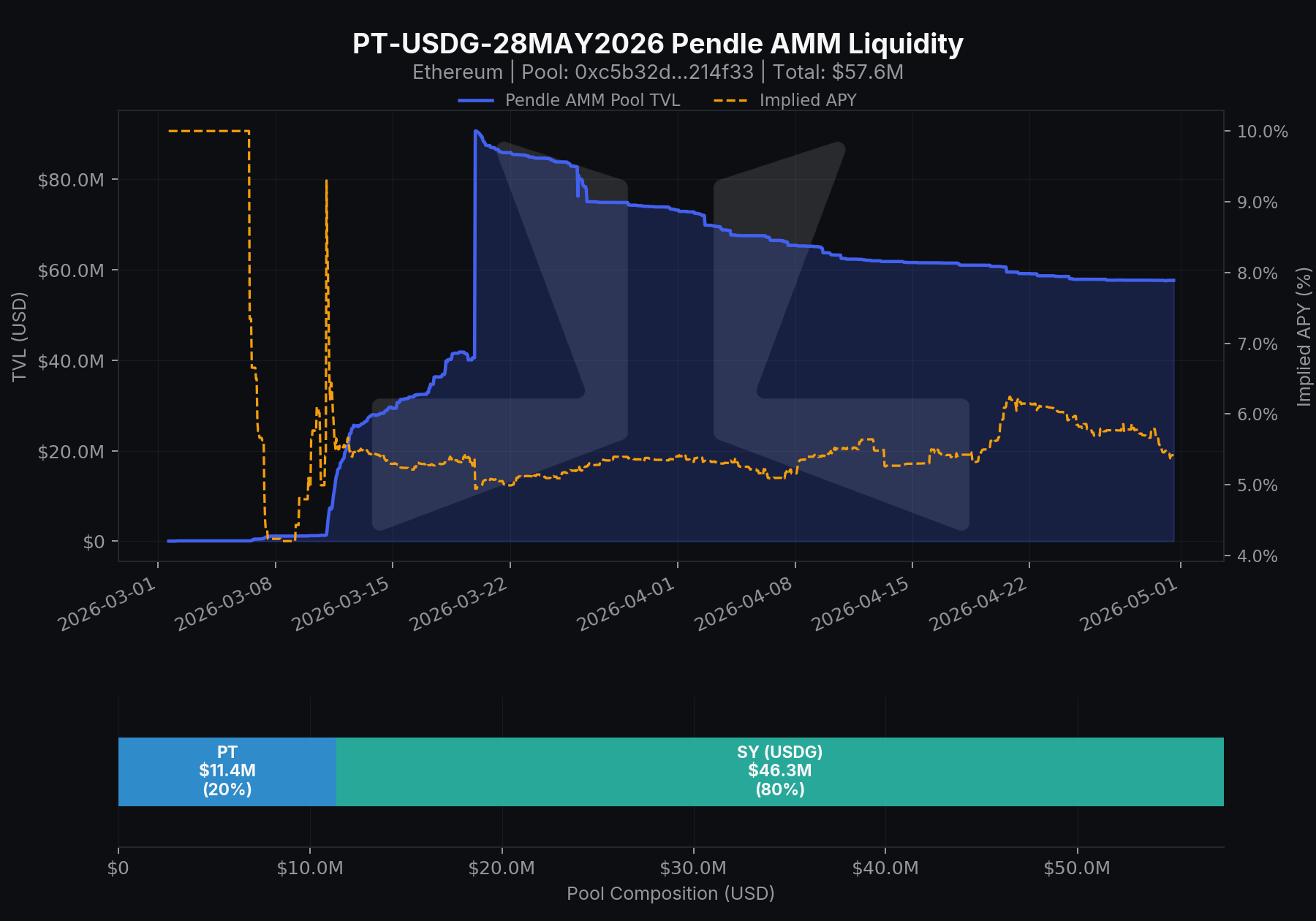

Liquidity

Source: LlamaRisk, April 30, 2026

The primary trading venue is the Pendle AMM pool on Ethereum, which holds $57.6M in total liquidity. The pool composition is 80% SY (USDG) / 20% PT, indicating ample depth on the SY side that supports orderly PT-to-USDG swaps. Pool TVL has remained broadly stable in the $55M to $80M range since mid-March, and the implied APY has compressed from the launch peak toward the 5% to 6% range as the maturity approaches.

Recommendation

Given persistent demand, the correlated collateral profile that anchors active borrowing, and ample Pendle AMM exit liquidity, we recommend doubling the supply cap from 40,000,000 to 80,000,000.

USD₮ (Aave V3 Celo)

USD₮ has reached 100.0% supply cap utilization (5,799,842 / 5,800,000) on the Aave V3 Celo instance. Borrow utilization sits at 34.9% (1,823,675 / 5,220,000).

Supply Distribution

Source: LlamaRisk, April 30, 2026

USD₮ supports a mixed usage profile on Celo: roughly half of the depicted top suppliers hold the asset on a passive deposit basis (HF infinite) and roughly half use it as collateral for short positions in other reserves (USDm, USDC, EURm, and a small WETH borrow). Health factors among active borrowers span 1.05 to 3.17 with most positions clustered between 1.05 and 1.25, consistent with stable-stable carry trades where collateral and debt are both USD-pegged. The collateral set in this chart contains only fiat-stable debt outside one ETH-denominated position, so peg-divergence loss bands remain narrow and well within the reserve’s liquidation bonus.

Recommendation

Given full supply cap utilization on a USD-pegged stablecoin reserve with active borrow demand on the Celo instance, we recommend doubling the supply cap from 5,800,000 to 11,600,000. The borrow cap remains unchanged.

xETH (Aave V3 X Layer)

xETH is currently at 84.7% borrow cap utilization (1,101 / 1,300) on the Aave V3 X Layer instance.

Borrow Distribution

Source: LlamaRisk, April 30, 2026

The dominant usage pattern is leveraged short ETH exposure funded by USDT0 collateral, alongside an ETH-correlated loop on a smaller position that pairs xBETH collateral against xETH debt. Health factors among active borrowers span 1.03 to 1.66 with the largest position at 1.30. The xBETH/xETH strategy is structurally correlated (both ETH-denominated), while the USDT0/xETH strategy carries directional ETH exposure for the borrower; the price-divergence channel remains bounded for the levered ETH LST looping strategy by X Layer’s ETH E-Mode parameters.

Recommendation

Given persistent borrow demand at the cap and a borrower set composed of correlated ETH carry and capped directional shorts, we recommend doubling the borrow cap from 1,300 to 2,600. The supply cap remains unchanged.

Cap Reductions on Borrow Caps

USDe on Aave V3 Ethereum sits at 10.2% borrow cap utilization (183M / 1.8B). The 1.8B borrow cap follows the yesterday’s supply cap reduction from 2,000,000,000 to 400,000,000, leaving a borrow ceiling materially above the new supply scale. The proposed cap of 360,000,000 is approximately 2x current outstanding borrow and aligns the borrow ceiling with the post-reduction supply scale.

WETH on Aave V3 Plasma sits at 6.5% borrow cap utilization (519 / 8,000). The 8,000 cap follows the yesterday’s supply cap reduction from 8,500 to 4,400. The proposed cap of 4,000 restores symmetric scaling between supply and borrow caps and remains approximately 7.7x current outstanding borrow.

USDe on Aave V3 Mantle sits at 18.5% borrow cap utilization (13.3M / 72M). The 72M borrow cap follows the yesterday’s supply cap reduction from 100,000,000 to 30,000,000, with current usage dominated by sUSDe-collateralized yield leveraging loops. The proposed cap of 27,000,000 is set at 90% of the 30,000,000 supply cap and sits at approximately 2x current outstanding borrow, preserving growth headroom for the looping demand on this instance.

Specification

Instance

Asset

Current Supply Cap

Recommended Supply Cap

Current Borrow Cap

Recommended Borrow Cap

Aave V3 MegaETH

USDe

50,000,000

100,000,000

40,000,000

unchanged

Aave V3 MegaETH

USDm

400,000,000

600,000,000

190,000,000

280,000,000

Aave V3 Ethereum Core

USDG

60,000,000

120,000,000

50,000,000

100,000,000

Aave V3 Ethereum Core

PT-USDG-28MAY2026

40,000,000

80,000,000

-

-

Aave V3 Celo

USD₮

5,800,000

11,600,000

5,220,000

unchanged

Aave V3 X Layer

xETH

unchanged (5,000)

unchanged (5,000)

1,300

2,600

Aave V3 Ethereum Core

USDe

unchanged (400,000,000)

unchanged (400,000,000)

1,800,000,000

360,000,000

Aave V3 Plasma

WETH

unchanged (4,400)

unchanged (4,400)

8,000

4,000

Aave V3 Mantle

USDe

unchanged (30,000,000)

unchanged (30,000,000)

72,000,000

27,000,000

Next Steps

We will move forward and implement these updates via the Risk Steward process.

Disclosure

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.

2 posts - 1 participant

Read full topic

LicenseN/A

Used Bygovernance.aave.com...

Mining PreferenceN/A

Integrity Proof